![]()

Advertiser Disclosure

Last update: June 6, 2025

6 minutes read

What Is a Disbursement in Student Loans? And How It Works

Learn what loan disbursement means, how student loans are disbursed and applied to your tuition and living expenses, and get actionable tips to manage and budget your aid effectively.

By Brian Flaherty, B.A. Economics

Edited by Rachel Lauren, B.A. in Business and Political Economy

Learn more about our editorial standards

By Brian Flaherty, B.A. Economics

Edited by Rachel Lauren, B.A. in Business and Political Economy

Learn more about our editorial standards

Navigating student loan disbursement is a critical part of managing your college finances—knowing when funds arrive, how they’re applied, and what to watch out for can save you from unexpected shortfalls or unnecessary debt.

If you’ve ever wondered "How are student loans disbursed?", this post will clarify what is disbursement and share practical tips for ensuring you get and use your funds responsibly. Discover how optimizing your loan strategies can benefit you when refinancing student loans.

Key takeaways

- Student loan disbursements are payouts of loan funds for covering educational expenses

- Understanding the difference between disbursement and drawdown can help in financial planning

- Practice the dos and don'ts to ensure responsible management of disbursed funds

What is a disbursement in student loans?

A disbursement in student loans is the process where loan funds are paid out to cover your educational expenses. It's an exciting moment because it means your financial aid plan is in action, supporting your college journey.

It's essential to know that a disbursement isn’t a one-time event. Federal and private student loans usually release funds in multiple installments throughout the academic year.

This strategy ensures the funds are used as intended - primarily for tuition and fees initially, followed by other educational expenses. Here’s an example breakdown of disbursement timing and purpose:

- First disbursement: Applied directly to tuition and school fees.

- Subsequent disbursements: Cover books, supplies, and living expenses.

This process centers around the school's financial aid office. They work with lenders to make sure the money is given out correctly.

After the initial costs are covered, any remaining amount is refunded to the student. This refund can support living expenses or buy essential academic materials.

TuitionHero Tip

It's important to keep an eye on each payment and how it affects the total amount you owe. Even though it might seem good to get extra money, remember that it adds to what you have to pay back later.

Disbursement vs. Drawdown

Understanding the subtle differences between disbursement and drawdown can significantly affect how you manage your education funds.

What is a disbursement?

A disbursement is when the money from a loan is given to your school or to you. It's like a transaction where the loan amount goes from the lender to you, mostly for educational costs. A typical example includes federal and private student loans being disbursed at the start of the semester.

What is a drawdown?

A drawdown happens when you take some money out of a larger amount. This term is often used with credit lines or retirement savings, but it also applies when you get money from your student loan.

For example, if you take out $10,000 from a $100,000 loan, it means you've received $10,000, and there's now $10,000 less in your total available funds, leaving you with a remaining $90,000.

Types of disbursement

Not all disbursements are created equal. The terms controlled and delayed disbursement come into play, affecting how funds flow and are used.

Controlled disbursement

This is a financial management tool that allows for the scheduling and release of funds in a careful way. Banks offer it as a service to their corporate clients, enabling them to manage cash flow efficiently by deciding the exact timing of disbursements.

Delayed disbursement

Also known as remote disbursement, this involves intentionally prolonging the payment process. Historically beneficial due to the lag in physical check processing, its use has decreased with the invention of electronic transfers.

Compare private student loans now

TuitionHero simplifies your student loan decision, with multiple top loans side-by-side.

Compare Rates

Dos and don'ts of managing student loan disbursements

Understanding how student loan disbursements work is important. Knowing the right steps to take and the ones to avoid can help you manage your loans better, reducing financial stress while you're in college and after you graduate.

Do

Do review disbursement notifications carefully. Understand the amount and timing.

Do use disbursement funds strictly for educational expenses. This ensures the loan serves its intended purpose.

Do keep track of each disbursement and its effect on your loan balance. Awareness is key to managing debt effectively.

Don't

Don't ignore communication from your lender or school. Missing out on key details can lead to surprises.

Don't spend loan disbursements on non-educational items. Misuse of funds can lead to financial issues later.

Don't lose sight of your overall loan balance. It's easy to overlook the cumulative effect of each disbursement.

What is a negative disbursement?

If you’re searching for a loan disbursement meaning, you’ll find it describes when funds are released—or later taken back—by your school or lender. A negative disbursement happens when a lender or your school takes back money previously sent to you.

This can occur if:

- Over‑award of aid: Your total grants, scholarships, and loans exceed your certified cost of attendance.

- Fee adjustments: Origination or administrative fees get reconciled after initial payout.

- Return of unearned funds: You withdraw from school or drop below half‑time and no longer qualify for the full amount.

Imagine you received a $5,000 refund for living expenses after tuition was covered. A month later, financial aid reviews your enrollment status and finds you weren’t full‑time—so they claw back $1,200.

This payment disbursement adjustment shows a $1,200 negative amount on your account, reducing your refund balance.

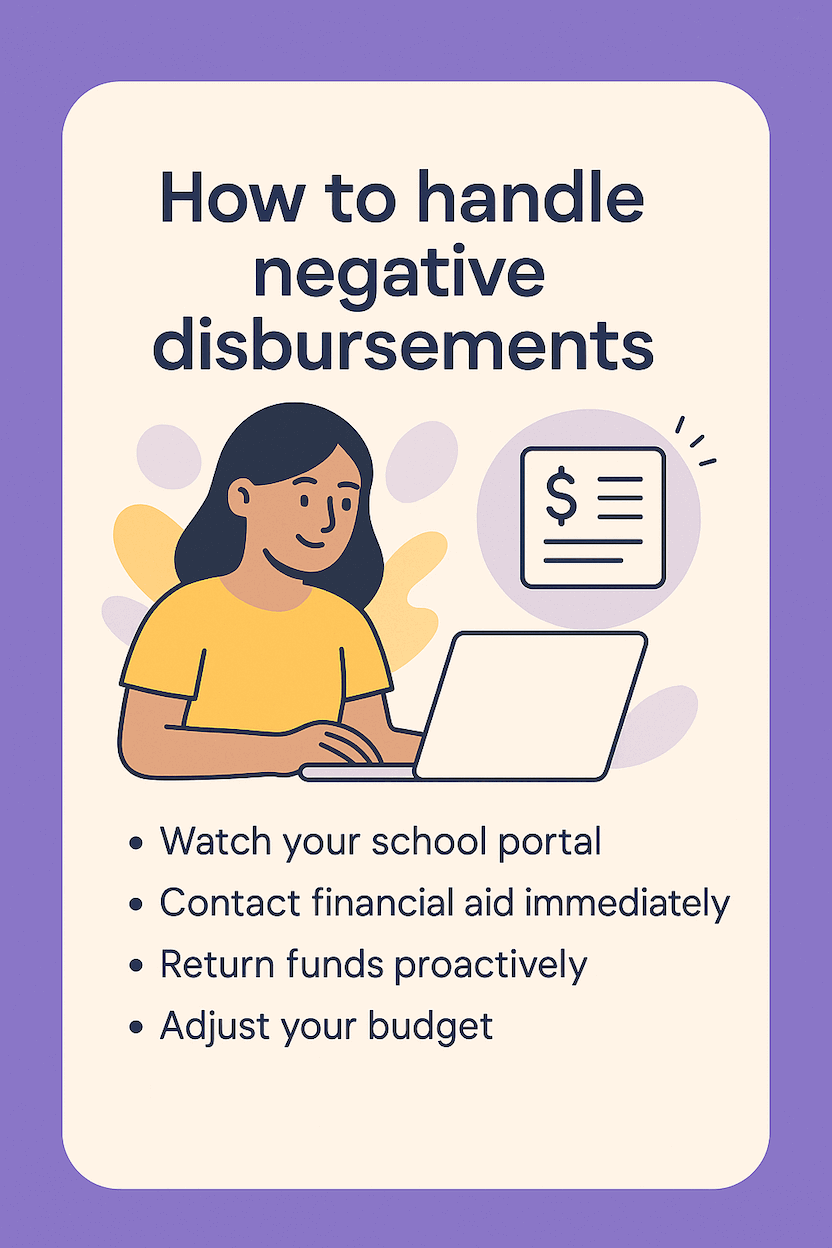

How to handle negative disbursements

- Watch your school portal: Set alerts for “pending charges” or “adjustments.”

- Contact financial aid immediately: Ask why funds were recouped and whether you can appeal or adjust enrollment.

- Return funds proactively: If you spot an over‑award before the school does, refund the excess to minimize claw‑back fees.

- Adjust your budget: Treat the reversal like an unexpected bill—shift spending or tap a small emergency fund if needed.

Why trust TuitionHero

At TuitionHero, we help with managing your student loans efficiently and finding scholarships. Check us out to handle your student loans well and possibly reduce the need for more loans.we also offer comprehensive advice on scholarships and credit card offers tailored for students.

Recent developments

Over the past month, the U.S. Department of Education announced that involuntary collections on defaulted loans will resume on May 5, 2025, after a five‑year pause, and authorized guaranty agencies to restart wage garnishment and other recovery actions.

At the same time, the Trump administration's major staff cuts in Federal Student Aid have thinned the ranks of those who certify enrollment and verify paperwork, potentially introducing new holds or delays in loan disbursement processes.

Meanwhile, Congress is debating a slate of reforms that would extend repayment terms to 30 years, eliminate certain forgiveness programs, and overhaul income‑driven repayment options—changes that could alter disbursement schedules for new borrowers

Frequently asked questions (FAQ)

Being smart about using your loan disbursement starts with a clear budget. Focus on essential expenses like tuition, books, and living costs.

Think ahead about the whole semester, and plan for unexpected costs. It's also wise to save some for emergencies.

If there's any left over after covering your educational needs, consider returning it to reduce your loan balance. For more on managing student loans, check out our student loan management resources.

Directly, loan disbursements don’t affect your credit score. However, how you use and repay your loans can have significant effects.

Using disbursements wisely and making timely repayments can positively influence your credit history. On the other hand, mishandling loan funds and accruing more debt than necessary, followed by late or missed payments, can hurt your credit score.

First, contact your school's financial aid office to understand the cause of the delay. It could be due to paperwork errors, processing delays, or verification issues.

Keeping open communication with your lender and the financial aid office is key. In the meantime, have a backup plan for covering immediate expenses, like using savings or a student-friendly credit card for urgent costs. At TuitionHero, we can help guide you through these challenges.

Yes—but usually not all at once and not always directly into your pocket. Federal and private student loans are often disbursed in installments tied to each term or semester.

Schools apply the funds to your bills first; only after tuition, fees, and housing charges are covered will any extra funds be refunded to you for living costs, books, or supplies.

Disbursement itself is neither inherently good nor bad—it’s simply the mechanism that puts your loan dollars to work. It’s good because it ensures your tuition gets paid on time and provides you access to necessary funds.

However, each disbursement increases your outstanding loan balance, so using the money wisely and keeping track of repayments is crucial to avoid excess debt.

Once your funds are released, your school applies them toward your tuition and any institutional charges. If there’s a surplus—say for living expenses or textbooks—the school issues you a refund via direct deposit or check.

Shortly thereafter, your lender sends you a repayment schedule detailing your first payment date, monthly amount, and any grace period. You can then plan your budget for the term ahead, knowing exactly how much aid you have and when your repayment obligation begins.

Final thoughts

By mastering the full disbursement process—from lender approval and school certification to refund timing—you’ll be better prepared for every payment cycle.

Whether you need clarity on how are private student loans disbursed, want to know how fast do student loans come in, or are curious on how do you receive student loan money, this knowledge keeps you in control.

Keep detailed records, monitor your account for adjustments, and act swiftly if funds are reversed—so your loans support your education, not your stress.

Source

Author

Brian Flaherty

Brian is a graduate of the University of Virginia where he earned a B.A. in Economics. After graduation, Brian spent four years working at a wealth management firm advising high-net-worth investors and institutions. During his time there, he passed the rigorous Series 65 exam and rose to a high-level strategy position.

Editor

Rachel Lauren

Rachel Lauren is the co-founder and COO of Debbie, a tech startup that offers an app to help people pay off their credit card debt for good through rewards and behavioral psychology. She was previously a venture capital investor at BDMI, as well as an equity research analyst at Credit Suisse.

At TuitionHero, we're not just passionate about our work - we take immense pride in it. Our dedicated team of writers diligently follows strict editorial standards, ensuring that every piece of content we publish is accurate, current, and highly valuable. We don't just strive for quality; we aim for excellence.

Related posts

While you're at it, here are some other college finance-related blog posts you might be interested in.

6 minutes read

What Are Pre-Orientation Programs?

Ever wondered how to make the most of your college start? Discover how pre-orientation programs can ease your transition and set you up for success before classes even begin.

Learn More

5 minutes read

How to Build a Strong Resume for Internships

Wondering how to craft a compelling internship resume that grabs attention? Discover essential strategies to build a standout resume and secure your dream internship.

Learn More

8 minutes read

How to Get Your Student Loans Forgiven

Learn how to erase student loan debt with our top strategies for Public Service Loan Forgiveness, including employer tips and payment plans.

Learn More

Shop and compare student financing options - 100% free!

Always free, always fast

TuitionHero is 100% free to use. Here, you can instantly view and compare multiple top lenders side-by-side.

Won’t affect credit score

Don’t worry – checking your rates with TuitionHero never impacts your credit score!

Safe and secure

We take your information's security seriously. We apply industry best practices to ensure your data is safe.

Finished scrolling? Start saving & find your private student loan rate today